Oracles

Every asset in a lending market relies on an oracle—an external data source that provides up-to-date prices onchain.

These prices are critical, as they determine:

- Borrowing power

- Loan-to-value (LTV)

- Liquidation conditions

Oracle data feeds directly into core protocol modules, including borrowing parameters and liquidation logic.

How Oracles Are Used

Each token in a market can use up to two oracle configurations:

- One for borrowing power (mLTV)

- One for solvency (liquidation thresholds)

This separation allows markets to:

- Be more capital efficient

- Maintain conservative solvency guarantees

Oracle Types

Silo supports multiple oracle pricing methodologies depending on the asset:

Market Price Oracles Aggregate prices across exchanges to produce a real-time market value.

Fundamental Oracles Price assets based on their underlying value rather than market price. Example: wstETH priced relative to ETH via its redemption ratio.

Reserve-Based Oracles Price assets based on redeemable reserves. Example: tBTC priced 1:1 with BTC based on backing.

Oracle Providers

Silo is oracle-agnostic.

Markets can integrate any oracle, and the protocol provides adapters for:

- Chainlink

- Redstone

- Pyth

- DIA

- ERC-4626 (vault-based pricing)

- Other custom implementations

Transparency & Risk Visibility

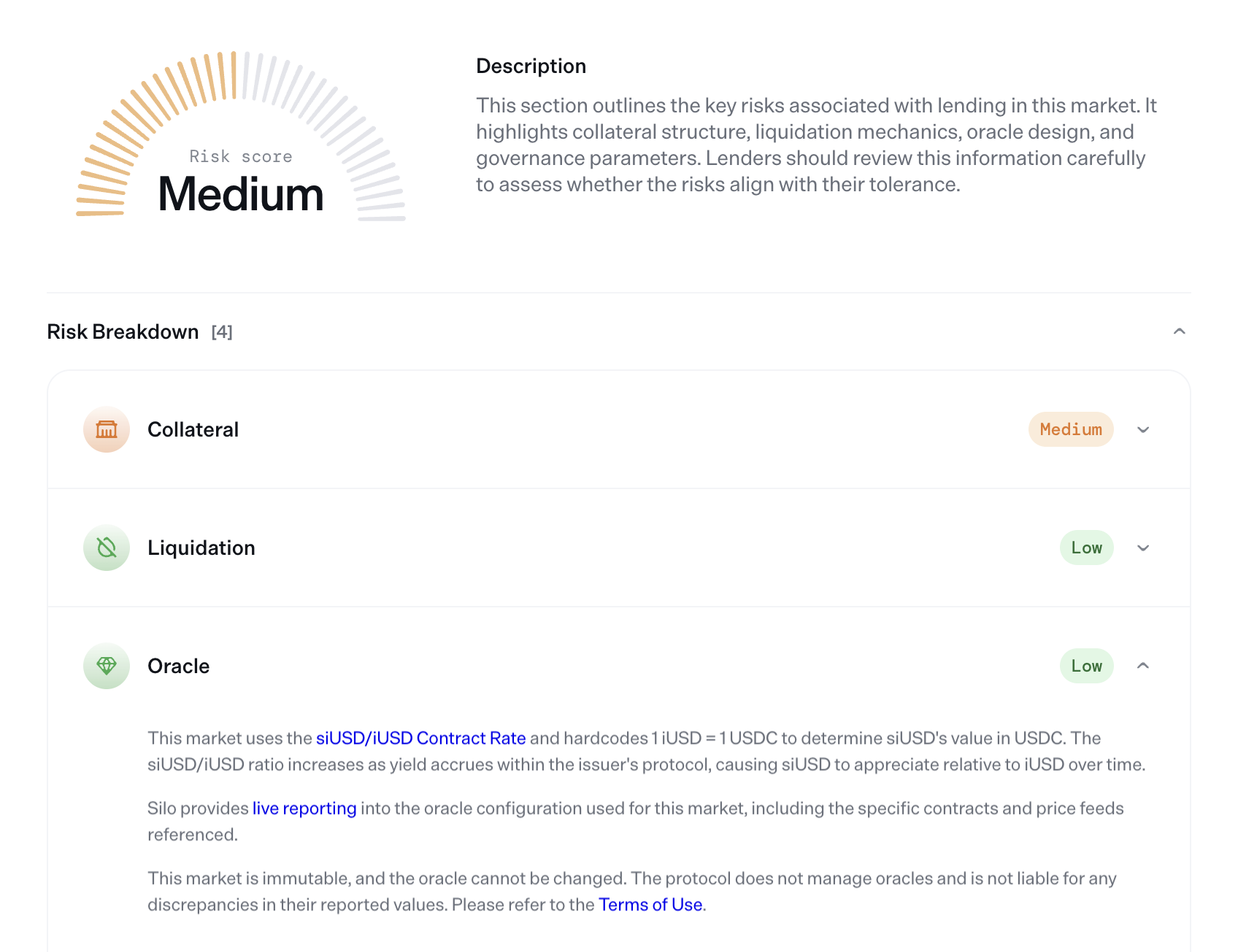

Silo provides a *omprehensive, real-time overview of all oracle configurations used in each market.

Users can inspect:

- Price sources for collateral and debt assets

- Oracle types and methodology

- Referenced contracts and feeds

This information is available directly in the Risk section of each market:

Disclaimer

Oracles are third-party systems that operate independently of the Silo Protocol.

- Silo does not control oracle providers or their data sources

- Oracle configurations are defined at market deployment and may be immutable

- The protocol is not responsible for inaccuracies, delays, or failures in oracle price reporting

Users should review oracle configurations carefully and understand the associated risks before participating in a market.